You have just discovered that your 401(k) account has dropped by 4.01%. Now you are wondering what to do and how to make the best of this situation. You can read on to learn more about the Tax implications of taking money out of your 401(k) before you turn 59 1/2. Although it can be confusing to see how the drop of 4.01% will affect your investment, remember that it is intended to grow.

4.01% drop in 401k balance

In the first quarter 2019, there was a decrease in the average retirement account balances. The 401(k) account balances have decreased to $121,700 on average, down from $127,100 in the fourth quarter of last year and $2,300 less than the first quarter of 2017. While this drop may not seem large, it represents a significant percentage of all retirement accounts and indicates that the workplace retirement plan is safer than cryptocurrency investment opportunities.

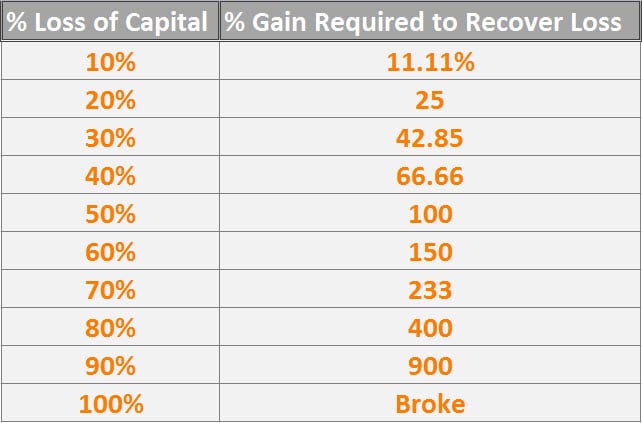

A drop of 4.01% in your 401(k), account can be both scary and disappointing. Your investment strategy may be questioned if your account balance starts to drop. This strategy may not align with your longterm goals. Before you rush to act, reflect on the larger picture. Although short-term losses can seem significant, historical data shows that short-term gains have more to compensate for short-term ones. You should only make portfolio changes if you are sure of your financial goals. Understanding your risk tolerance is a way to ease your worries during bear markets.

Diversification

You might be in your thirties and forties and wondering what you can do to protect your retirement account. While the stock market is subject to ups and falls, most 401 (k) plans are designed in order to protect your money from major losses. Your 401(k), which is your retirement account, should be invested in diversified funds to spread out the risk among different assets. You can still invest in stocks with your plan, but you should diversify the portfolio with mutual funds and exchange traded funds.

If you are still unsure whether diversification is worth the effort, keep in mind that stocks or bonds are susceptible to losing money, even during bull times. This is only temporary. The U.S. stock markets have declined on average 14% per yr since 1979. Yet, 83% in that time period have seen positive returns. These losses can be very frustrating, but they don't have the power to stop you from achieving your investment goals. Diversification can make your investments more resilient against market swings.

Tax implications

You might think that dropping your 401k plan is an easy decision, but you should be aware of the tax consequences. The 10% additional tax you might be charged if your money is withdrawn early could apply to you. This is a incentive to employees to continue to participate in their employer's retirement plan. Additionally, taxes will apply to federal income that is withdrawn and applicable state taxes. If you have just begun your career and have little debt, you may want to consider dropping your 401k account and looking for other ways to access your cash. You should also consider lifestyle inflation when making your decision.

Your income and other circumstances may impact the tax consequences of closing your 401(k). If you're using the money to replace your income, you may be in the same tax bracket as if you used the money. If you live on less income, your tax bracket will be lower. The less income you have, the less taxes you'll owe.

You can withdraw money from your retirement plan before the age of 59 1/2

Taking money out of a 401(k) before age 59 1/2 is a common mistake that carries hefty penalties. It is not a wise decision to withdraw money from your 401(k) prior to the deadline. However, there are many reasons you might want it delayed. One reason is that you could lose the tax advantage. There are other reasons to delay it, such as to gain as much money before your retirement.

To withdraw money from your 401 (k), you will need to wait until you turn 59 1/2. There are several exceptions to the early withdrawal rule. You might be able to get distributions even if you are retired. You don't have to withdraw your funds early if you take them over your life expectancy or the life expectancy for a beneficiary.

FAQ

Which fund is best suited for beginners?

When you are investing, it is crucial that you only invest in what you are best at. FXCM offers an online broker which can help you trade forex. They offer free training and support, which is essential if you want to learn how to trade successfully.

If you feel unsure about using an online broker, it is worth looking for a local location where you can speak with a trader. You can also ask questions directly to the trader and they can help with all aspects.

Next would be to select a platform to trade. CFD platforms and Forex are two options traders often have trouble choosing. Both types trading involve speculation. Forex does have some advantages over CFDs. Forex involves actual currency trading, while CFDs simply track price movements for stocks.

Forex makes it easier to predict future trends better than CFDs.

Forex trading can be extremely volatile and potentially risky. CFDs are a better option for traders than Forex.

We recommend you start off with Forex. However, once you become comfortable with it we recommend moving on to CFDs.

What type of investment has the highest return?

It doesn't matter what you think. It depends on how much risk you are willing to take. You can imagine that if you invested $1000 today, and expected a 10% annual rate, then $1100 would be available after one year. If you were to invest $100,000 today but expect a 20% annual yield (which is risky), you would get $200,000 after five year.

In general, the higher the return, the more risk is involved.

It is therefore safer to invest in low-risk investments, such as CDs or bank account.

However, it will probably result in lower returns.

Investments that are high-risk can bring you large returns.

For example, investing all your savings into stocks can potentially result in a 100% gain. But it could also mean losing everything if stocks crash.

Which one do you prefer?

It all depends upon your goals.

If you are planning to retire in the next 30 years, and you need to start saving for retirement, it is a smart idea to begin saving now to make sure you don't run short.

But if you're looking to build wealth over time, it might make more sense to invest in high-risk investments because they can help you reach your long-term goals faster.

Be aware that riskier investments often yield greater potential rewards.

There is no guarantee that you will achieve those rewards.

What are the types of investments available?

There are many options for investments today.

These are the most in-demand:

-

Stocks - Shares of a company that trades publicly on a stock exchange.

-

Bonds - A loan between two parties secured against the borrower's future earnings.

-

Real estate is property owned by another person than the owner.

-

Options – Contracts allow the buyer to choose between buying shares at a fixed rate and purchasing them within a time frame.

-

Commodities: Raw materials such oil, gold, and silver.

-

Precious metals: Gold, silver and platinum.

-

Foreign currencies - Currencies outside of the U.S. dollar.

-

Cash - Money deposited in banks.

-

Treasury bills are short-term government debt.

-

A business issue of commercial paper or debt.

-

Mortgages - Loans made by financial institutions to individuals.

-

Mutual Funds – Investment vehicles that pool money from investors to distribute it among different securities.

-

ETFs - Exchange-traded funds are similar to mutual funds, except that ETFs do not charge sales commissions.

-

Index funds - An investment fund that tracks the performance of a particular market sector or group of sectors.

-

Leverage is the use of borrowed money in order to boost returns.

-

ETFs (Exchange Traded Funds) - An exchange-traded mutual fund is a type that trades on the same exchange as any other security.

These funds are great because they provide diversification benefits.

Diversification means that you can invest in multiple assets, instead of just one.

This will protect you against losing one investment.

Statistics

- Over time, the index has returned about 10 percent annually. (bankrate.com)

- Most banks offer CDs at a return of less than 2% per year, which is not even enough to keep up with inflation. (ruleoneinvesting.com)

- 0.25% management fee $0 $500 Free career counseling plus loan discounts with a qualifying deposit Up to 1 year of free management with a qualifying deposit Get a $50 customer bonus when you fund your first taxable Investment Account (nerdwallet.com)

- They charge a small fee for portfolio management, generally around 0.25% of your account balance. (nerdwallet.com)

External Links

How To

How to properly save money for retirement

Retirement planning involves planning your finances in order to be able to live comfortably after the end of your working life. It is the time you plan how much money to save up for retirement (usually 65). It is also important to consider how much you will spend on retirement. This includes hobbies, travel, and health care costs.

You don't need to do everything. Many financial experts can help you figure out what kind of savings strategy works best for you. They'll examine your current situation and goals as well as any unique circumstances that could impact your ability to reach your goals.

There are two main types of retirement plans: traditional and Roth. Roth plans allow you to set aside pre-tax dollars while traditional retirement plans use pretax dollars. You can choose to pay higher taxes now or lower later.

Traditional Retirement Plans

Traditional IRAs allow you to contribute pretax income. You can contribute up to 59 1/2 years if you are younger than 50. If you want your contributions to continue, you must withdraw funds. You can't contribute to the account after you reach 70 1/2.

If you've already started saving, you might be eligible for a pension. These pensions can vary depending on your location. Matching programs are offered by some employers that match employee contributions dollar to dollar. Others provide defined benefit plans that guarantee a certain amount of monthly payments.

Roth Retirement Plans

Roth IRAs allow you to pay taxes before depositing money. Once you reach retirement, you can then withdraw your earnings tax-free. There are however some restrictions. For medical expenses, you can not take withdrawals.

A 401(k), or another type, is another retirement plan. These benefits may be available through payroll deductions. Employees typically get extra benefits such as employer match programs.

401(k), plans

Most employers offer 401k plan options. They allow you to put money into an account managed and maintained by your company. Your employer will automatically contribute a percentage of each paycheck.

You decide how the money is distributed after retirement. The money will grow over time. Many people prefer to take their entire sum at once. Others distribute their balances over the course of their lives.

Other types of Savings Accounts

Other types are available from some companies. TD Ameritrade has a ShareBuilder Account. With this account you can invest in stocks or ETFs, mutual funds and many other investments. Additionally, all balances can be credited with interest.

Ally Bank allows you to open a MySavings Account. You can deposit cash and checks as well as debit cards, credit cards and bank cards through this account. You can then transfer money between accounts and add money from other sources.

What's Next

Once you've decided on the best savings plan for you it's time you start investing. Find a reputable investment company first. Ask friends and family about their experiences working with reputable investment firms. For more information about companies, you can also check out online reviews.

Next, figure out how much money to save. This step involves figuring out your net worth. Net worth refers to assets such as your house, investments, and retirement funds. It also includes liabilities, such as debts owed lenders.

Divide your net worth by 25 once you have it. That is the amount that you need to save every single month to reach your goal.

If your net worth is $100,000, and you plan to retire at 65, then you will need to save $4,000 each year.