Tax havens are places that offer low tax rates, or even no effective tax rates, and financial secrecy. Many wealthy individuals and business entities use these jurisdictions to structure their business operations and protect their personal assets. Many jurisdictions enjoy a great reputation. However, there are some that have negative consequences. You can find tax havens in the following list for business purposes. These jurisdictions offer low- or zero-tax rates, financial secrecy as well as a lack of transparency.

Financial centers offshore

An offshore jurisdiction is a country and/or jurisdiction that provides financial service to nonresidents in a way that is different from its domestic economy. It has a low rate of tax and a small government. Many financial services can be obtained without the need for residents' personal information. For privacy reasons, these centers are often used to make investments. There are also a number of benefits to these centers that may outweigh the disadvantages of using them.

Low or zero tax rates

The United States has a very interesting and unique tax situation. Every state has their own tax laws. Each state also imposes its own income tax rates. This makes the United States a tax haven because individuals are able to avoid paying taxes in their own countries. Because they don't have income tax, some states are tax havens. It means that Americans living in the US may use the tax haven to buy a home.

Lack of transparency

The EU's blacklist identifying tax havens is an important tool in fighting money laundering. However, it lacks transparency. EU member states did not include all tax havens including Guernsey and Cayman Islands. Eight countries are now on the tax havens list, but none of them meet the criteria needed to be considered tax havens.

Offshore credit

To combat tax havens and tax evasion, the EU created a list of tax havens to counter the spread of these tax havens. These tax havens provide tax evasion and avoidance opportunities by concealing the proceeds of criminal or illegal activities. EU created a list because it was concerned about tax practices that could harm citizens and businesses. These practices result from the difference between the global reach of financial flow and the geographic scope of jurisdictions.

Conduit OFCs

The European Parliament supported the CORPNET approach for mapping tax havens. Gabriel Zucman demonstrated that the Orbis database underestimates Ireland's conduit OFC. The Zucman/Torslov/Wier list places Ireland as the biggest conduit OFC. These lists mirror the most popular academic top ten tax havens lists.

FAQ

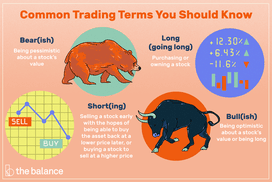

Should I buy mutual funds or individual stocks?

You can diversify your portfolio by using mutual funds.

They may not be suitable for everyone.

For example, if you want to make quick profits, you shouldn't invest in them.

Instead, pick individual stocks.

Individual stocks allow you to have greater control over your investments.

Additionally, it is possible to find low-cost online index funds. These allow you track different markets without incurring high fees.

What investments are best for beginners?

Investors who are just starting out should invest in their own capital. They must learn how to properly manage their money. Learn how retirement planning works. How to budget. Learn how to research stocks. Learn how to interpret financial statements. How to avoid frauds Learn how to make sound decisions. Learn how to diversify. Learn how to protect against inflation. How to live within one's means. Learn how to save money. Learn how to have fun while you do all of this. It will amaze you at the things you can do when you have control over your finances.

What type of investment has the highest return?

It doesn't matter what you think. It depends on how much risk you are willing to take. For example, if you invest $1000 today and expect a 10% annual rate of return, then you would have $1100 after one year. If you were to invest $100,000 today but expect a 20% annual yield (which is risky), you would get $200,000 after five year.

In general, the higher the return, the more risk is involved.

So, it is safer to invest in low risk investments such as bank accounts or CDs.

However, you will likely see lower returns.

High-risk investments, on the other hand can yield large gains.

For example, investing all of your savings into stocks could potentially lead to a 100% gain. But it could also mean losing everything if stocks crash.

Which one is better?

It all depends on your goals.

You can save money for retirement by putting aside money now if your goal is to retire in 30.

High-risk investments can be a better option if your goal is to build wealth over the long-term. They will allow you to reach your long-term goals more quickly.

Remember: Higher potential rewards often come with higher risk investments.

But there's no guarantee that you'll be able to achieve those rewards.

Do I require an IRA or not?

An Individual Retirement Account (IRA) is a retirement account that lets you save tax-free.

You can save money by contributing after-tax dollars to your IRA to help you grow wealth faster. These IRAs also offer tax benefits for money that you withdraw later.

IRAs can be particularly helpful to those who are self employed or work for small firms.

In addition, many employers offer their employees matching contributions to their own accounts. Employers that offer matching contributions will help you save twice as money.

Statistics

- An important note to remember is that a bond may only net you a 3% return on your money over multiple years. (ruleoneinvesting.com)

- As a general rule of thumb, you want to aim to invest a total of 10% to 15% of your income each year for retirement — your employer match counts toward that goal. (nerdwallet.com)

- They charge a small fee for portfolio management, generally around 0.25% of your account balance. (nerdwallet.com)

- Some traders typically risk 2-5% of their capital based on any particular trade. (investopedia.com)

External Links

How To

How to Retire early and properly save money

Retirement planning involves planning your finances in order to be able to live comfortably after the end of your working life. It's when you plan how much money you want to have saved up at retirement age (usually 65). You should also consider how much you want to spend during retirement. This includes hobbies, travel, and health care costs.

It's not necessary to do everything by yourself. A variety of financial professionals can help you decide which type of savings strategy is right for you. They will examine your goals and current situation to determine if you are able to achieve them.

There are two main types, traditional and Roth, of retirement plans. Roth plans allow you put aside post-tax money while traditional retirement plans use pretax funds. You can choose to pay higher taxes now or lower later.

Traditional Retirement Plans

A traditional IRA lets you contribute pretax income to the plan. You can make contributions up to the age of 59 1/2 if your younger than 50. If you want to contribute, you can start taking out funds. The account can be closed once you turn 70 1/2.

A pension is possible for those who have already saved. These pensions are dependent on where you work. Employers may offer matching programs which match employee contributions dollar-for-dollar. Other employers offer defined benefit programs that guarantee a fixed amount of monthly payments.

Roth Retirement Plan

Roth IRAs do not require you to pay taxes prior to putting money in. Once you reach retirement age, earnings can be withdrawn tax-free. There are restrictions. There are some limitations. You can't withdraw money for medical expenses.

Another type is the 401(k). These benefits are often offered by employers through payroll deductions. Employer match programs are another benefit that employees often receive.

401(k).

Most employers offer 401k plan options. You can put money in an account managed by your company with them. Your employer will automatically contribute to a percentage of your paycheck.

The money grows over time, and you decide how it gets distributed at retirement. Many people decide to withdraw their entire amount at once. Others distribute their balances over the course of their lives.

Other types of savings accounts

Some companies offer additional types of savings accounts. TD Ameritrade offers a ShareBuilder account. With this account, you can invest in stocks, ETFs, mutual funds, and more. In addition, you will earn interest on all your balances.

At Ally Bank, you can open a MySavings Account. This account can be used to deposit cash or checks, as well debit cards, credit cards, and debit cards. You can then transfer money between accounts and add money from other sources.

What's Next

Once you have decided which savings plan is best for you, you can start investing. First, find a reputable investment firm. Ask family members and friends for their experience with recommended firms. For more information about companies, you can also check out online reviews.

Next, determine how much you should save. Next, calculate your net worth. Net worth refers to assets such as your house, investments, and retirement funds. It also includes debts such as those owed to creditors.

Once you know your net worth, divide it by 25. This number is the amount of money you will need to save each month in order to reach your goal.

For example, if your total net worth is $100,000 and you want to retire when you're 65, you'll need to save $4,000 annually.